$RDX.AX Redox Pty Ltd a potential compounder in a fragmented market.

Investment Thesis

In the current market landscape, characterized by uncertainty, geopolitical tensions, inflation, and fluctuating interest rates, I am identifying numerous promising opportunities for building a long-term investment portfolio. However, I remain concerned that many companies are not trading at a sufficient margin of safety, which is a critical factor in my investment strategy.

Redox may exemplify this situation; although its stock price has dropped from $4.50 to $2.77, I suspect there could be further declines ahead. Nonetheless, I recognize that high-quality companies typically do not offer substantial margins of safety and Redox may be starting to approach a good area to buy in.

In this analysis, I aim to clarify any uncertainties surrounding the company.

About the company

Redox operates as a supplier and distributor of chemical products, ingredients, and raw materials. The company maintains a prominent position in Australia and New Zealand, with some presence in Malaysia, and is currently seeking to expand its operations into the United States.

What captivates me about Redox is its status as a market leader in Australia, despite holding only a 3% market share. This indicates the market's fragmentation and suggests that Redox has significant opportunities for growth, whether through organic development or mergers and acquisitions.

In addition to its leadership in Australia, Redox ranks as the 13th largest company in the Asia-Pacific region and 34th on a global scale.

Redox was established in 1965 in Sydney by Ronald Coneliano, who is the father of the current CEO and managing director, Raimond Coneliano. Further details about the family will be discussed in the shareholders section.

Talking about the products Redox distributes we can find:

Organic commodity chemicals such as: Organic salts, Hydrocarbons & Alcohols.

Inorganic commodiy chemicals such as: Mineral and other salts, Concrete and cement additives, Acids, Alkalis and oxides.

Specialty chemicals such as: Ingredients, antioxidants, rheology modifiers, UV stabilisers, specialty coatings…

Plastic rubbers such as: Polyethylene, Polypropylene, Plastic film & Synthetic rubbers

Others such as: Proteins, starches, vitamins & amino acids.

And refering to the industries served by Redox, we can find:

Human health and nutrition

Crop production and protection

Plastics, rubber and foam

Industrial

Animal Health and nutrition

Household and personal care

Surface coatings

Mining and explosive

Watercare

The market

Redox functions within one of the largest sectors globally, as indicated by the World Health Organization, which ranks the chemical industry as the second-largest manufacturing sector worldwide. According to a study by Frost & Sullivan, referenced during the company's IPO, total global chemical sales reached approximately $6.3 trillion in 2021 and are projected to grow to $10 trillion by 2030. However, this figure does not represent the total addressable market (TAM) relevant to Redox. As previously mentioned, Redox acts as a distributor, serving as an intermediary between manufacturers who prefer not to manage the complexities of product distribution and the end clients.

In terms of the distribution segment within the chemical industry, it was valued at $425 billion in 2021, with only 9% attributed to third-party distributors like Redox, suggesting a TAM of around $38 billion.

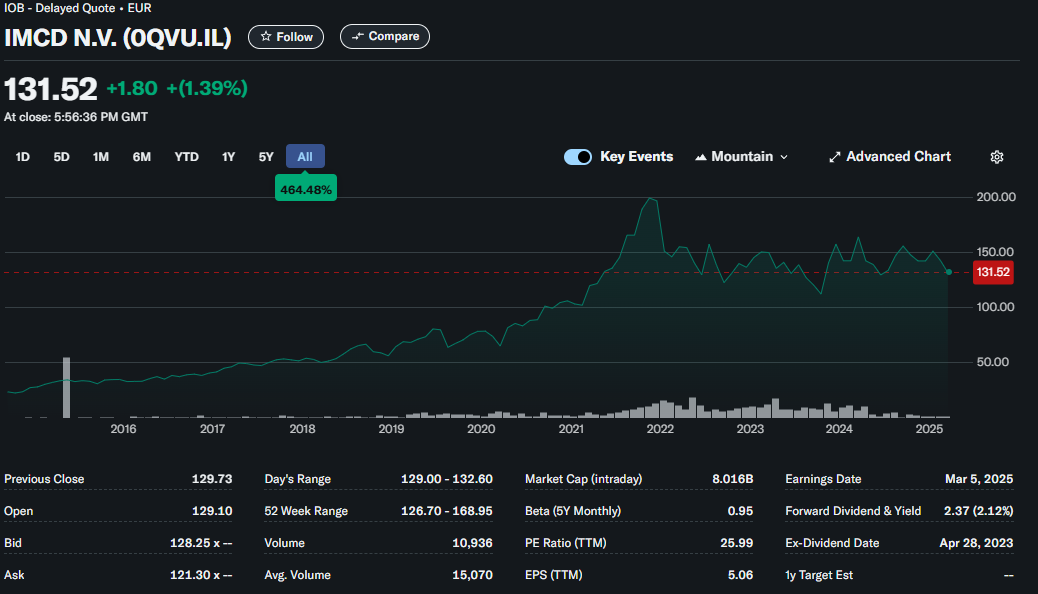

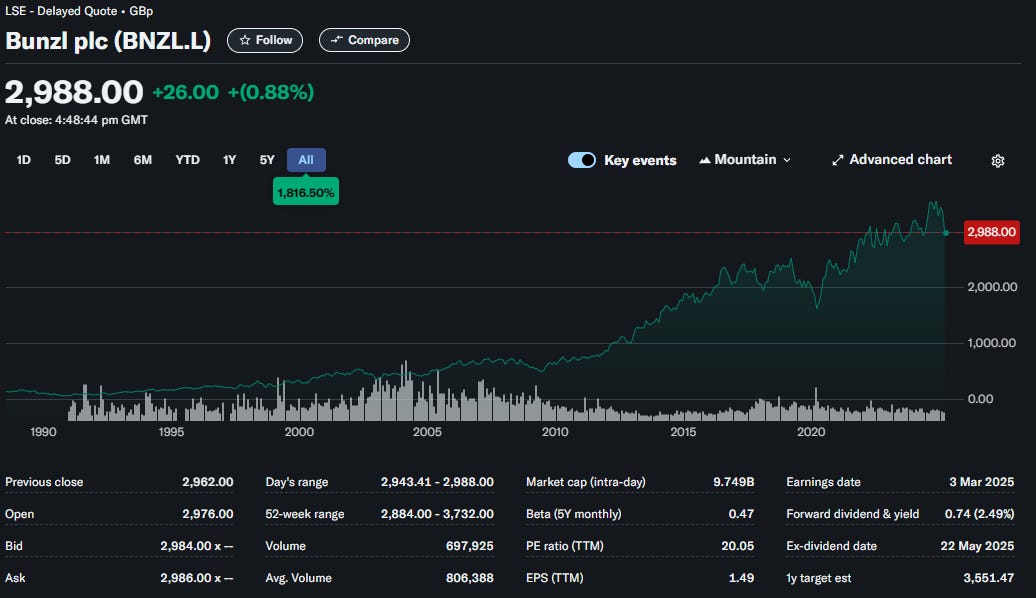

The global market is notably fragmented, with over 10,000 distributors in operation. The top 3 global distributors have just 9% of market share. The peers we can compare Redox with are Brenntag, Univar Solutions, IMCD, DSHK and Azelis. In Australia and New Zealand, the chemical markets heavily rely on imports, underscoring the critical role of well-established distributors.

I recognize that distributor players typically face low barriers to entry, as evidenced by the existence of approximately 10,000 distributors in the global chemical market. However, I will outline several factors that could assist Redox in solidifying its leading position.

Regulatory licenses for certain chemical products

Scale and supply chain management

Working capital demands

Exclusive contracts

The chemical industry is characterized by complex and continually changing regulations, necessitating that Redox secures the necessary permits and approvals to facilitate ongoing business growth.

Logistics are crucial to Redox's business model, particularly since Australia and New Zealand primarily rely on imports. Delays in international shipping can lead to shortages and increased prices, ultimately impacting Redox's profit margins. This situation has recently compelled Redox to enhance its working capital through debt financing.

With Trump´s arrival to the White House, and tariffs playing and important role, this can affect Redox international expansion in the US as trade restrictions might arise. We will contemplate this, during the valuation.

History

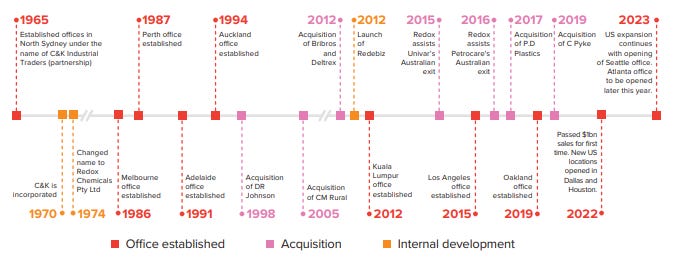

Founded in 1965 as a chemical distributor with a focus on European suppliers, Redox diversified its global supply base during the 1980s, strengthening its presence in Australia through the creation of its own distribution centers. By the 1990s, it began importing dry and liquid bulk products, which increased its competitiveness and market share in Australia. In 1994, it expanded its operations to New Zealand, establishing a network of three branches covering both islands and part of the Pacific. In 2012, it made an international leap by opening an office in Kuala Lumpur, Malaysia, consolidating its access to Asian markets and regional sources of supply.

In 2012, Redox boosted its growth with the strategic acquisition of Bribros and Deltrex, companies that expanded its portfolio in plastics, foams and logistics capacity, in addition to adding specialized equipment. That same year, it developed Redebiz, an integrated management system (CRM/ERP) that optimized the monitoring of markets, costs and regulatory compliance. In 2015, it began its U.S. expansion with an office in Los Angeles, followed by locations in Oakland (2019), Dallas, Houston (2022) and Seattle (2023), with plans for Atlanta. These actions reflect its focus on organic growth, strategic acquisitions and technology, positioned in the U.S. market.

Business Model

Redox is the leading player in chemical distribution in Australia with just a 3% market share. Redox has more than 900 suppliers and 6400 customers which leads into more than 580.000 tonnes sold and 23.000 containers handled.

Redox operations consist of negotiation with overseas suppliers, obtain bulk purchase rates, arrange international shipping, negotiate regulatory requirements, warehouse and storage, mixing, blending, filling packaging and labelling.

Sales Model

Forward Order Sales – accounts for approximately 26.1% of sales. These sales are where a customer contracts with Redox to source product(s) on its behalf for a specific quantity on a specified delivery date. Redox will already have or will then identify a global source for the product(s), obtain multiple quotes for purchase and delivery of the product(s) to the customer, select the best quote and then offer a price to the customer based on the quotes received and internal costs associated with making the sale. The purchase price will be hedged using forward exchange contracts, ensuring that Redox minimises any foreign exchange risk or inventory holding risk on the sale.

Master Order Sales – accounts for approximately 58.5% of sales. These sales are where a customer requests Redox to source product(s) on its behalf and indicates that it is prepared to enter into a contract for multiple deliveries, usually for an agreed total volume over a specified period of time. The price is usually set on or around the date of entering into the contract. Redox will already have or will then identify global sources for the product(s), obtain quotes for purchase and delivery of the product(s) to the customer, select the best quote and then offer a price to the customer based on market rates prevailing at the time and with due consideration to logistics and other associated costs.

Ex-Inventory Sales – accounts for approximately 15.4% of sales. These sales are where Redox will build up inventory in its warehouses to satisfy ongoing daily demand from non-contracted customers who prefer not to, or do not have the scale to, contract with Redox on a forward sales order or master sales order basis. Often these sales are made to smaller customers, or to any customers who need products within a short time frame

Redox has 8 in-house managed warehouses and +100 externally managed sites over 4 countries, the eight in-house managed facilities provide Redox with capacity of over 65,000 pallets, this facilities are leased from Ceneda a related party under the control of owner and CEO Robert Coneliano. Redox incurs lease payments exceeding 7 million to Ceneda, warranting scrutiny to ensure that management is not benefiting disproportionately from these transactions compared to the core business operations.

Redox sources its products from international supply partners that adhere to specific licensing and accreditation criteria. A significant portion of its sales consists of contracted agreements, where the sales team engages in price negotiations with both customers and manufacturers. As Redox continues to expand, its negotiating leverage with manufacturers is expected to increase.

Over the past three decades, the company has achieved an average growth rate of 11.9%. However, in FY24, revenue experienced a decline of 9%, and growth in H125 has not met expectations.

Product sales are spread across various sectors, as are both the customer and supplier bases, indicating that Redox is not reliant on any specific supplier, customer, or sector.

Redox has over 6,400 customers from approximately 170 different industries. Its customers range from small and medium sized businesses to listed global corporations. There are no individually material customer contracts.

Sourcing from a diversified supplier base provides Redox with the stability of supply, cost efficiencies and differentiated product offerings which Management believes ensures Redox retains a strong competitive advantage in the market

Shareholders & Management

One positive indicator I look for when evaluating a company is the extent to which management has a personal stake in its success. In this particular case, family members hold a significant portion of the company's shares, amounting to over 45%. Specifically, Richard and Robert own 13.43% and 10.12% of the shares, respectively.

Raimond Conelliano: is the Chief Executive Officer and Managing Director after having served as a Director on the Board of Redox for ten years, he´s had +27 career in Redox. Owns 13.003.236 shares and has stock options totalling 700.000.

Renato Conelliano: is the Executive Director and Marketing Director, he joined Redox in 1980. He has had many roles over time including both sales and product management responsibilities. Owns 63.171.503 shares and has stock options totalling 300.000.

Richard Conelliano: he is Alternate Director and Chief Operating Officer, began his career as a computer programmer at Redox 29 years ago, where he has made significant contributions to the Company's success. His most notable achievement has been his role, along with others, in the development of Redox’s integrated ERP/CRM software platform Redebiz. Owns 79.596.183 shares and has 300.000 shares in options.

Raimond, Renato, and Richard receive fixed salaries of $800,000, $500,000, and $401,651, respectively. This structure emphasizes the significance of their variable compensation in stock options, as it incentivizes them to enhance shareholder value, aligning their interests with those of the shareholders.

The objective of this performance rights is Total Shareholder Return relative to the performance of the S&P/ASX 300 Index over the period (July 1st 2023 to June 30th 2027). Target awards are to be above 50th percentile which will redeem 50% and above 75th percentile of the index will award 100% of the vesting.

Personally I don´t like this rewarding method as I don´t see it directly reflected to company numbers and shareholder returns.

Management has implemented a payout ratio strategy ranging from 60% to 80% of net income. In my view, this approach is concerning for a company with significant acquisition opportunities, as I believe it is not an effective means of enhancing shareholder value.

Peers

If you go to your broker you will see that Redox has been recently listed at the ASX in 2023, so you might want to check how comparable companies have devoloped in the stock market. We can find several peers such as Brenntag, Bunzl, DKSH, IMCD, Ixom & Univar Solutions.

Brenntag

Established in 1874 in Mülheim, Germany, as a modest family enterprise focused on coal and basic chemicals, Brenntag has transformed into the premier global distributor of specialty chemicals and ingredients. With its headquarters in Essen, Germany, and listed on the Frankfurt Stock Exchange, the company employs over 18,000 individuals and operates across 72 countries. It serves as a vital link between major chemical manufacturers like BASF and Dow and a wide range of industrial clients in sectors including food, pharmaceuticals, and agriculture. Brenntag's business model integrates sophisticated logistics, strategic warehousing, and tailored technical services, solidifying its role as a crucial component of global supply chains. Like Redox, Brenntag engages with a diverse array of industries. In Europe, which accounts for 40% of its revenue, the company is particularly noted for its distribution of automotive and manufacturing chemicals. In the Americas, contributing 35% of revenues, it excels in the energy and agriculture sectors, while in the Asia-Pacific region, which represents 20% of its revenue, it leverages growth in the pharmaceutical and electronics markets. Key segments of its operations include industrial chemicals, food and nutrition, pharmaceuticals, and agriculture.

NTM EV/EBITDA = 7,86

NTM P/E = 12.61

NTM MC/FCF = 0.75

5.6% operating margin

IMCD

Established in 1995 in Rotterdam, The Netherlands, IMCD has become a formidable player in the distribution of specialty ingredients and high-value chemicals, effectively competing with traditional companies like Brenntag through its agile, niche-focused strategy. The company is publicly traded on the Amsterdam Stock Exchange (ticker: IMCD) and operates in over 60 countries, employing 4,300 individuals. IMCD concentrates on sectors where innovation and technical knowledge are essential, including pharmaceuticals, cosmetics, premium food, and advanced materials. Its business model, which emphasizes strategic alliances with specialized suppliers and tailored services, has allowed it to achieve margins that surpass the industry average, solidifying its status as a leader in high-growth markets. In contrast to Brenntag, which has a history that stretches back to the 19th century, IMCD is a relatively young enterprise that has experienced rapid growth. Initially starting as a local chemical distributor in the Netherlands, the company underwent significant transformation in the 2010s. After its initial public offering in 2014, IMCD embarked on an aggressive acquisition strategy, purchasing over 50 companies from 2015 to 2023, particularly enhancing its presence in the cosmetics ingredients sector. This strategy has facilitated its expansion into markets such as North America and Asia-Pacific, with a consistent focus on acquiring companies that possess technically sophisticated portfolios and access to high-end customers.

IMCD avoids competing in commoditized markets. Instead, it concentrates on segments where the added value-whether technical, regulatory or logistical-justifies high margins: Personal care and cosmetics, Pharmaceuticals, Functional food, Advanced materials.

NTM EV/EBITDA = 14.15

NTM P/E = 19.54

NTM MC/FCF = 1.87

8.9% operating margin

Bunzl

Founded in 1854 in Vienna as a small ribbon and textile retailer, Bunzl has evolved into a global B2B distribution colossus, although its name rarely resonates with the general public. Headquartered in London and listed on the FTSE 100 (LSE: BNZL), the company operates in 32 countries, employs more than 22,000 people and generates annual revenues in excess of £12 billion (2023). Its business model is based on supplying essential non-strategic products - from disposable packaging to safety equipment - to sectors such as catering, healthcare and industrial cleaning, it has grown by acquisitions: since 1980, it has integrated more than 200 companies, from local glove distributors in Mexico to surgical equipment suppliers in Australia. Main segments: foodservice, cleaning, healthcare, retail.

NTM EV/EBITDA = 9.69

NTM P/E = 14.72

NTM MC/FCF = 13.33

8% operating margin.

Brenntag and IMCD serve as the most appropriate benchmarks for comparing Redox, as both primarily function within the chemical sector. Notably, Brenntag's product portfolio exhibits greater seasonality due to its significant exposure to industries such as automotive, resulting in lower profit margins compared to Redox and IMCD.

This peer comparison reveals that Redox is not the sole company experiencing growth through acquisitions; rather, this trend is prevalent across the entire sector.

Valuation

I believe Redox has the potential to become a serial acquirer due to the vast fragmented market that offers significant growth opportunities. This positions the company well for long-term success. However, in the short term, the valuation remains high, and current market conditions and geopolitical factors could pose challenges. For instance, Redox may encounter difficulties in executing its growth strategy in the United States.

Redox presently holds a cash reserve of 57 million AUD alongside a debt of 18 million, creating an excellent opportunity to acquire new companies at favorable valuations amid these challenging market conditions.

Neutral

In my neutral scenario, I have projected the expected performance for FY25 based on the results from H125, during which the company experienced a decline in revenues in the USA while witnessing a rebound in sales in the APAC region. For FY26 and FY27, I have forecasted a 5% growth across all regions. Regarding cost estimates, I have utilized historical levels for my modeling.

By utilizing a price-to-earnings (PER) ratio of 15, which I consider reasonable for a market leader operating in a fragmented market with significant growth prospects, I project an upside of 17% from the current price to $3.26.

Optimistic

In my optimistic projection, I anticipate a 10% growth in both Australia and the USA, aiming for a more favorable outlook in the short-term environment along with slightly improved cost margin estimates.

By applying a price-to-earnings (PER) ratio of 20, which aligns with the upper range of historical performance consistent with a growth narrative, I calculate an upside potential of 86%, bringing the target price to $5.18.

Pesimistic

In the pessimistic outlook, I anticipate a decline in revenue for FY25 and FY26, followed by a modest recovery in FY27.

Utilizing a price-to-earnings (P/E) ratio of 12, which is quite reasonable given the current potential challenges facing the company, I arrive at a valuation of $2.21, indicating a potential downside of 20%.

Conclusion

Recent declines in stock prices have presented me with the opportunity to initiate a position in this company. I maintain the view that further decreases in share prices are possible if market conditions continue to deteriorate.

However, I believe this is an appropriate entry point, with the possibility of an increase in the portfolio percentage if the downward trend persists and if there are no significant changes within Redox.

I would prefer to see the company adopt a more aggressive approach to mergers and acquisitions, rather than focusing primarily (60% to 80%) on dividends.

Additionally, the management's stock compensation could be optimised, I want them to earn more, but, we must see results.

With strategic acquisitions, I am confident that this company has the potential to become a strong performer in the coming years.

Disclaimer

All the content in this post is for informational purposes only and do not represent a financial advice. You should do your own research and due diligence.

I have a long position on Redox.

Interesting writeup. What's your thoughts on the share price now? Is it enough margin of safety for you? Did you average down?